One of the biggest expenses for any business can be Workers Compensation Insurance. Knowing this, business owners and managers have a strong motivation to find ways to save on this expense while also protecting the company’s assets and mitigating risks. When navigating this often-confusing landscape, one of the most important components to consider is the “Experience Modification Rate”, or X Mod (also known as the experience modification, experience modification rating, EMR, X Mod, XMod, the mod, and more).

The X Mod can be thought of like a credit score, but instead of determining the interest rate an individual will pay for a loan, it instead is the driving factor that determines the premium a business is going to be charged by an insurance company. But unlike a credit score, a business should seek to lower their X-Mod, and institute policies and practices to keep it low.

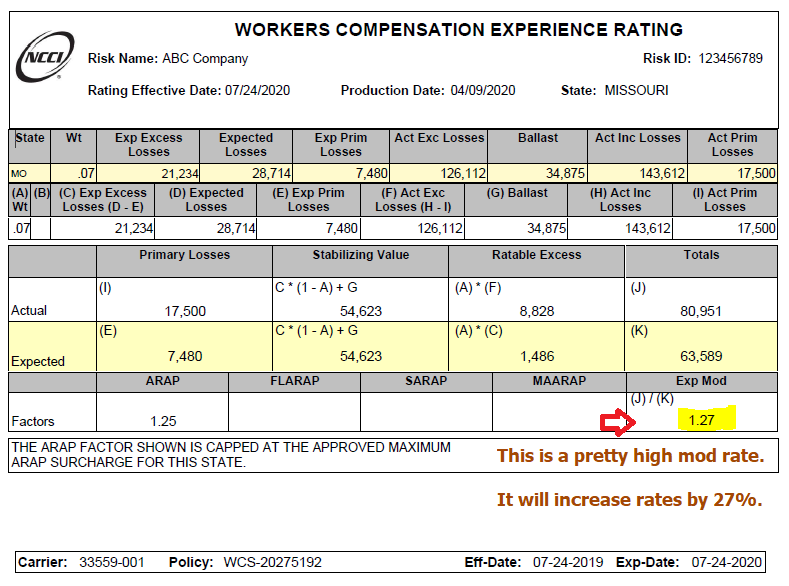

The X-Mod give insurers an indication of the potential risks and financial losses associated with offering a particular business workers’ comp coverage. If your business has an XMod of 100%, the premium amount will not be adjusted up or down by the insurance provider.However, if a company has an experience modification rate of 125%, then they will be assessed an increase in premium of 25%. So a company with $5,000 in workers compensation premiums will now pay $6,250. Whereas, a company with an 80% xmod will now pay $4,250

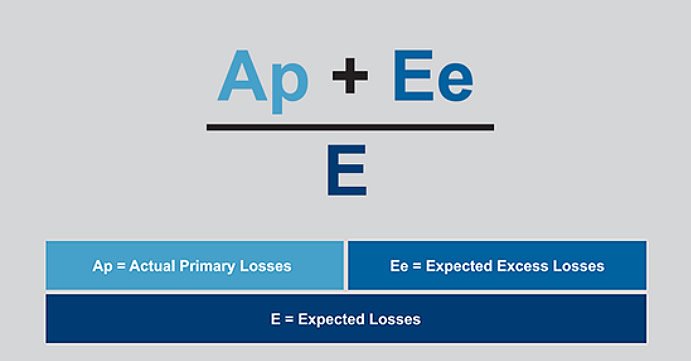

When a rating bureau calculates your X-Mod, it compares your actual losses to your expected losses. Your actual losses are the losses you've actually sustained. Your expected losses are a statistical estimate of the losses your insurance company is likely to pay for a business assigned your class codes. If your actual losses exceed your expected losses by a significant amount, your X-Mod will likely exceed 1.0.

Some workers' compensation claims may be denied if an investigation indicates an injury or illness is caused by an incident that is not covered. Some injuries that are typically not covered by workers' compensation include:

With us, you have access to top notch carriers and competitive pricing. We do...

We provide various coverage options which may be available to best protect ...

What good is insurance if you have to haggle over claims if something happens...

We provide various coverage options which may be available to best protect ...

If you’re wondering how you can control your X-mod, there are a few ways. We can help manage your risks with the following measures:

Once you’re able to identify the things that are going to affect your X-mod, it’s time to apply them. Get in touch with us now to manage your X-Mod efficiently.

Let us levarage and manage your EMR to get more lucrative deals from insurance companies

Copyright © 2022 Laurence Taylor. All Rights Reserved.

Call Now:

Call Now: